Understanding how hard inquiries impact your credit score is crucial for anyone looking to maintain or improve their financial health. Hard inquiries can significantly affect your creditworthiness, and knowing how they work can help you make smarter financial decisions. In this article, we will delve deep into the mechanics of hard inquiries, their effects on your credit score, and how you can manage them effectively.

Whether you're applying for a credit card, a mortgage, or a personal loan, financial institutions often perform a hard inquiry to assess your creditworthiness. These inquiries are recorded on your credit report and can influence your credit score. As such, it's important to be informed about how many hard inquiries can affect your credit score and what steps you can take to mitigate potential damage.

This guide will provide actionable insights and expert advice to help you navigate the complexities of hard inquiries. From understanding the basics to exploring strategies for managing your credit score, we'll cover everything you need to know to protect your financial future.

Read also:Discover The Sweet World Of Cookie Jam A Comprehensive Guide

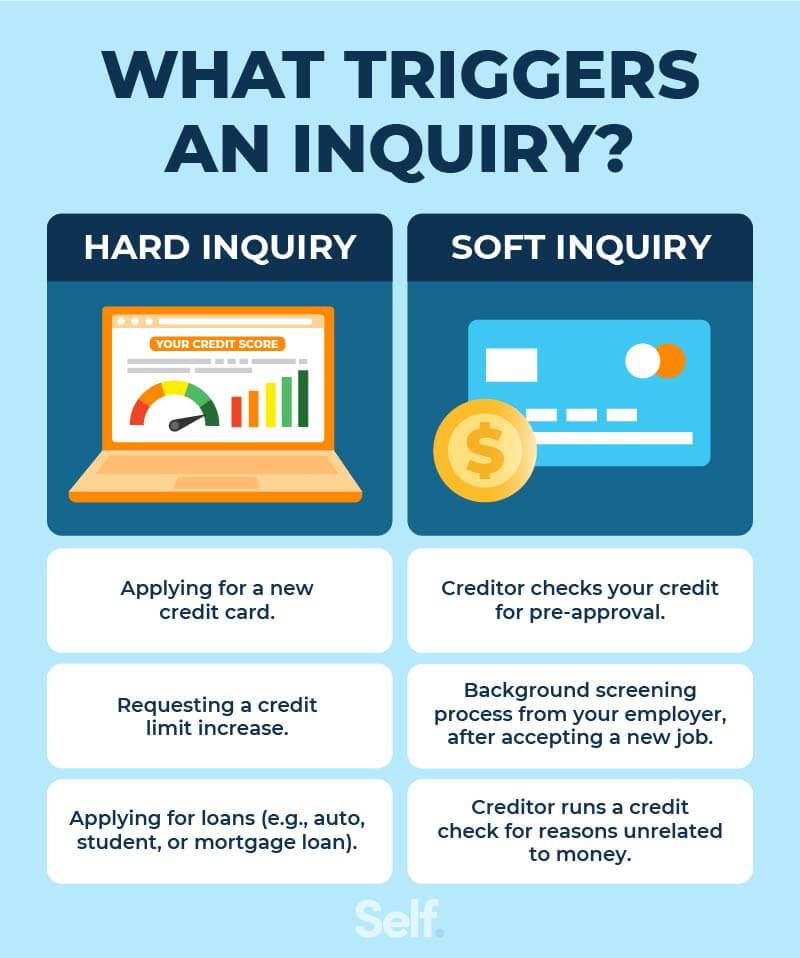

What Are Hard Inquiries?

Hard inquiries occur when a lender or creditor checks your credit report as part of a formal credit application process. Unlike soft inquiries, which do not affect your credit score, hard inquiries can have a measurable impact on your credit standing. These inquiries are typically initiated when you apply for credit products like loans, credit cards, or mortgages.

Each hard inquiry is recorded on your credit report and can remain visible for up to two years. While the impact on your credit score diminishes over time, multiple hard inquiries within a short period can raise concerns about your financial stability and creditworthiness. It's essential to understand how and when hard inquiries are made to minimize their effect.

How Many Hard Inquiries Can Affect Your Credit Score?

The number of hard inquiries that can affect your credit score varies depending on the credit scoring model used. On average, each hard inquiry can lower your credit score by up to five points. However, the exact impact depends on several factors, including:

- Your overall credit history

- The number of recent inquiries

- The type of credit product applied for

- Your existing credit mix and utilization

For individuals with shorter credit histories or fewer credit accounts, the impact of hard inquiries may be more pronounced. Conversely, those with long-standing credit histories and diverse credit portfolios may experience less significant effects.

How Hard Inquiries Affect Your Credit Score

Factors Influencing the Impact

Several factors influence how much hard inquiries affect your credit score:

- Credit History Length: Longer credit histories tend to absorb the impact of hard inquiries better.

- Credit Utilization: High credit utilization rates can amplify the negative effects of hard inquiries.

- Recent Credit Applications: Multiple recent applications can signal financial distress to lenders.

Short-Term vs. Long-Term Effects

Hard inquiries primarily impact your credit score in the short term. While they remain on your credit report for two years, their effect typically diminishes after the first year. Most credit scoring models focus on recent activity, meaning older inquiries have less influence over time.

Read also:Understanding Calories In Wingstop A Complete Guide To Nutritional Insights

Strategies to Minimize the Impact of Hard Inquiries

Shop Around Responsibly

When shopping for loans or credit cards, it's important to conduct your research within a limited time frame. Many credit scoring models treat multiple inquiries for the same type of credit (e.g., auto loans or mortgages) within a 14-45 day window as a single inquiry. This approach allows you to compare rates without significantly impacting your credit score.

Limit Unnecessary Applications

Avoid applying for multiple credit products unnecessarily. Each application triggers a hard inquiry, which can cumulatively harm your credit score. Prioritize your financial needs and only apply for credit when it's truly necessary.

Understanding Credit Scoring Models

FICO vs. VantageScore

Two primary credit scoring models are widely used: FICO and VantageScore. Both models consider hard inquiries, but their methodologies differ slightly. FICO scores generally deduct fewer points for hard inquiries compared to VantageScore. Understanding the nuances of these models can help you better manage your credit profile.

Key Differences in Scoring

- FICO scores focus more on payment history and credit utilization.

- VantageScore places greater emphasis on recent credit activity and inquiries.

Steps to Protect Your Credit Score

Monitor Your Credit Report

Regularly reviewing your credit report is essential for maintaining a healthy credit score. You can obtain a free credit report annually from each of the three major credit bureaus (Equifax, Experian, and TransUnion). Look for unauthorized hard inquiries and dispute any inaccuracies promptly.

Improve Credit Utilization

Keeping your credit utilization ratio below 30% can offset the negative effects of hard inquiries. Paying down existing balances and avoiding maxing out credit cards can improve your overall credit health.

Common Misconceptions About Hard Inquiries

Many people harbor misconceptions about hard inquiries and their impact on credit scores. Here are a few common myths debunked:

- Myth: All credit checks are hard inquiries. Fact: Only formal credit applications trigger hard inquiries. Checking your own credit or pre-approval offers typically result in soft inquiries.

- Myth: Hard inquiries always harm your credit score. Fact: While hard inquiries can lower your score, their impact is often minimal and temporary.

How to Dispute Unauthorized Hard Inquiries

If you discover unauthorized hard inquiries on your credit report, you have the right to dispute them. Follow these steps to remove inaccurate inquiries:

- Contact the creditor associated with the inquiry and request verification.

- If the inquiry is indeed unauthorized, file a dispute with the credit bureau.

- Provide supporting documentation to expedite the resolution process.

Conclusion: Taking Control of Your Credit Health

In summary, hard inquiries can affect your credit score, but their impact is often manageable with the right strategies. By understanding how many hard inquiries affect credit score and adopting responsible credit practices, you can safeguard your financial well-being. Remember to:

- Limit unnecessary credit applications.

- Shop around responsibly within a limited time frame.

- Monitor your credit report regularly for inaccuracies.

We encourage you to take action by reviewing your credit report today and implementing the strategies discussed in this guide. Share your thoughts or questions in the comments below, and explore our other articles for more insights into credit management and financial health.

Table of Contents

- What Are Hard Inquiries?

- How Many Hard Inquiries Can Affect Your Credit Score?

- How Hard Inquiries Affect Your Credit Score

- Strategies to Minimize the Impact of Hard Inquiries

- Understanding Credit Scoring Models

- Steps to Protect Your Credit Score

- Common Misconceptions About Hard Inquiries

- How to Dispute Unauthorized Hard Inquiries

- Conclusion: Taking Control of Your Credit Health