Loans are an essential financial tool that can help individuals and businesses achieve their goals. Whether you're planning to buy a house, start a business, or manage unexpected expenses, understanding the benefits of a loan is crucial. Loans provide flexibility and empower people to make important life decisions without being constrained by immediate cash flow limitations.

In today's fast-paced world, loans have become a common solution for various financial requirements. From personal loans to mortgages, they cater to different needs and offer tailored solutions. By understanding the advantages, you can make informed decisions about borrowing and effectively manage your finances.

This article delves into the top benefits of a loan, providing actionable insights and expert advice to help you navigate the borrowing process confidently. Whether you're new to loans or looking to expand your financial knowledge, this guide will serve as a valuable resource.

Read also:Remarkable Story Of Conjoined Twins Brittany And Abby A Journey Of Separation And Triumph

Table of Contents

- What is a Loan?

- Types of Loans

- Benefits of a Loan

- Improved Financial Accessibility

- Flexibility in Use

- Interest Rate Considerations

- How Loans Build Credit

- Credit Score Impact

- Responsible Borrowing

- Loans for Business Growth

- Startup Funding

- Expansion Capital

- Loans for Personal Needs

- Home Purchases

- Education Funding

- Conclusion

What is a Loan?

A loan is a financial agreement where one party borrows money from another with the promise to repay it, typically with interest, over a specified period. Loans can be secured or unsecured, depending on whether collateral is required. Secured loans, such as mortgages, require assets like property as collateral, while unsecured loans, like personal loans, rely on the borrower's creditworthiness.

Understanding the mechanics of loans is essential for making informed decisions. From repayment terms to interest rates, each loan has unique features designed to meet specific financial needs. By familiarizing yourself with these aspects, you can better assess which loan option suits your situation best.

Types of Loans

There are various types of loans available, each tailored to specific purposes. Some common examples include:

- Mortgage Loans: Used to purchase real estate properties, these loans often have long repayment terms.

- Personal Loans: Offered for general purposes, personal loans can cover expenses like medical bills or vacations.

- Business Loans: Designed to support entrepreneurs and small business owners, these loans help with startup costs or expansion.

- Auto Loans: Specifically for purchasing vehicles, auto loans come with fixed repayment schedules.

Choosing the right type of loan depends on your financial goals and current circumstances. It’s important to evaluate your needs carefully before committing to any borrowing agreement.

Benefits of a Loan

Loans offer numerous benefits that can significantly enhance your financial capabilities. One of the primary advantages is access to immediate funds, which allows you to tackle emergencies or seize opportunities without delay. Additionally, loans provide structure to your financial planning by establishing clear repayment terms and interest rates.

Another key benefit is the potential to improve your credit score. By consistently making timely payments, you demonstrate financial responsibility, which lenders appreciate. This can lead to better borrowing terms in the future and increased access to credit when needed.

Read also:Reveal The Marvels Of Arikytsya Erom A Comprehensive Insight

Improved Financial Accessibility

Flexibility in Use

One of the standout benefits of a loan is the flexibility it offers. Whether you need funds for personal or business purposes, loans can be tailored to fit your specific needs. For instance, a personal loan might allow you to consolidate debt, while a business loan could fund a new marketing campaign.

Interest Rate Considerations

Interest rates play a crucial role in determining the overall cost of a loan. Fixed interest rates provide stability, ensuring that your monthly payments remain consistent throughout the loan term. On the other hand, variable interest rates may offer lower initial costs but carry the risk of increasing over time. Understanding these differences helps you choose the most cost-effective option.

How Loans Build Credit

Taking out a loan can positively impact your credit score if managed responsibly. Each timely payment contributes to a strong credit history, which lenders use to assess your reliability. Over time, this can lead to better loan terms, lower interest rates, and increased borrowing limits.

Credit Score Impact

Your credit score is influenced by several factors, including payment history, credit utilization, and length of credit history. Loans contribute to all these areas, providing a comprehensive way to build credit. However, it's crucial to avoid over-borrowing, as excessive debt can negatively affect your score.

Responsible Borrowing

Responsible borrowing involves borrowing only what you can afford to repay. This practice not only protects your credit score but also ensures financial stability. By creating a realistic budget and sticking to it, you can manage your loan obligations effectively and avoid unnecessary stress.

Loans for Business Growth

For entrepreneurs and business owners, loans are a vital tool for growth and expansion. They provide the necessary capital to invest in new technologies, hire additional staff, or enter new markets. Without loans, many businesses would struggle to scale and remain competitive.

Startup Funding

Starting a business often requires significant upfront investment. Loans offer a reliable source of startup funding, enabling entrepreneurs to acquire essential resources and establish a strong foundation. With the right loan, you can turn your business idea into a thriving reality.

Expansion Capital

As businesses grow, they often need additional capital to support expansion efforts. Loans provide the necessary funds to increase production, enhance marketing strategies, or acquire new facilities. By leveraging loans for expansion, businesses can achieve sustained growth and improve profitability.

Loans for Personal Needs

Loans aren’t just for businesses; they also cater to personal financial needs. From purchasing a home to funding education, loans offer solutions for various life milestones. By understanding the options available, you can make the most of these financial tools.

Home Purchases

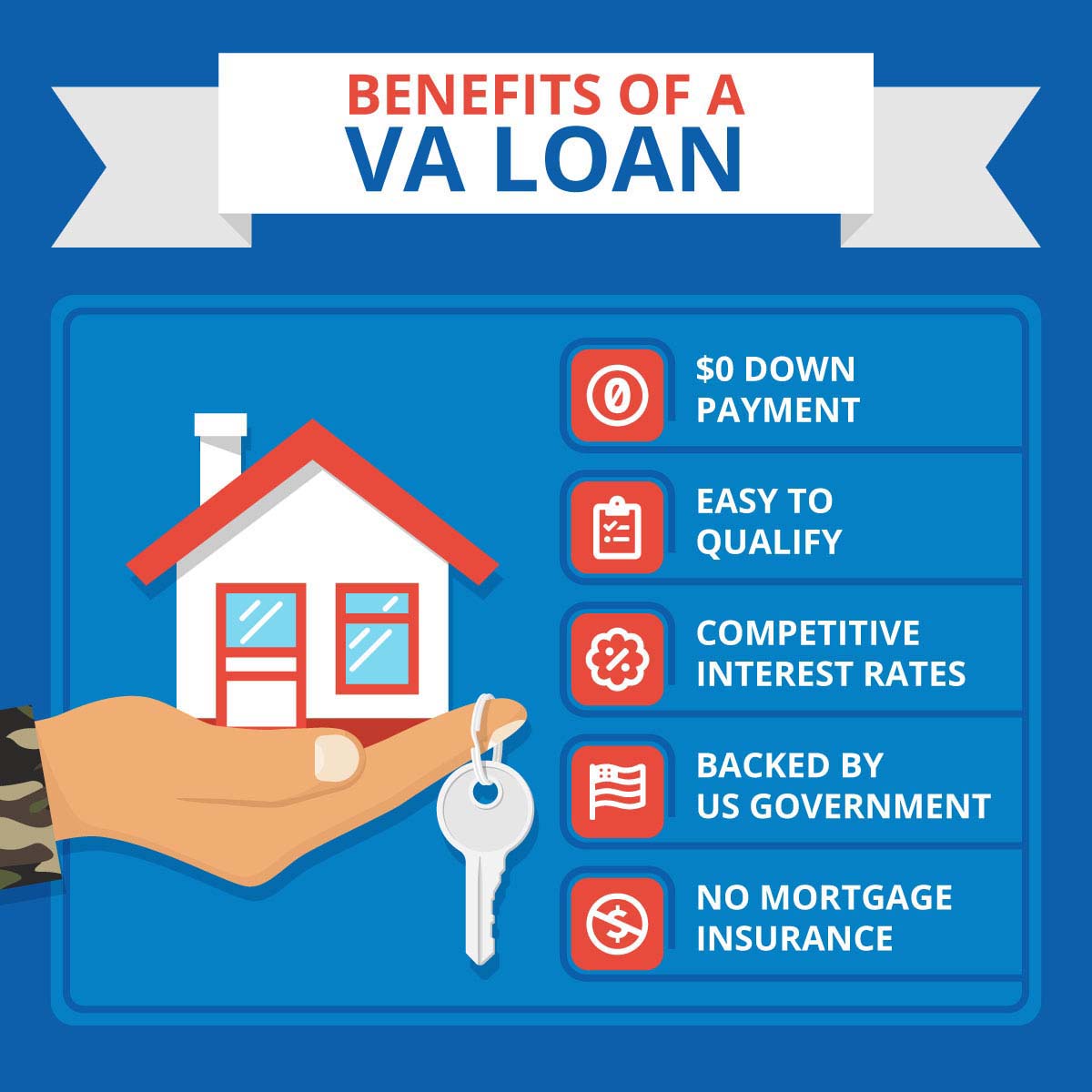

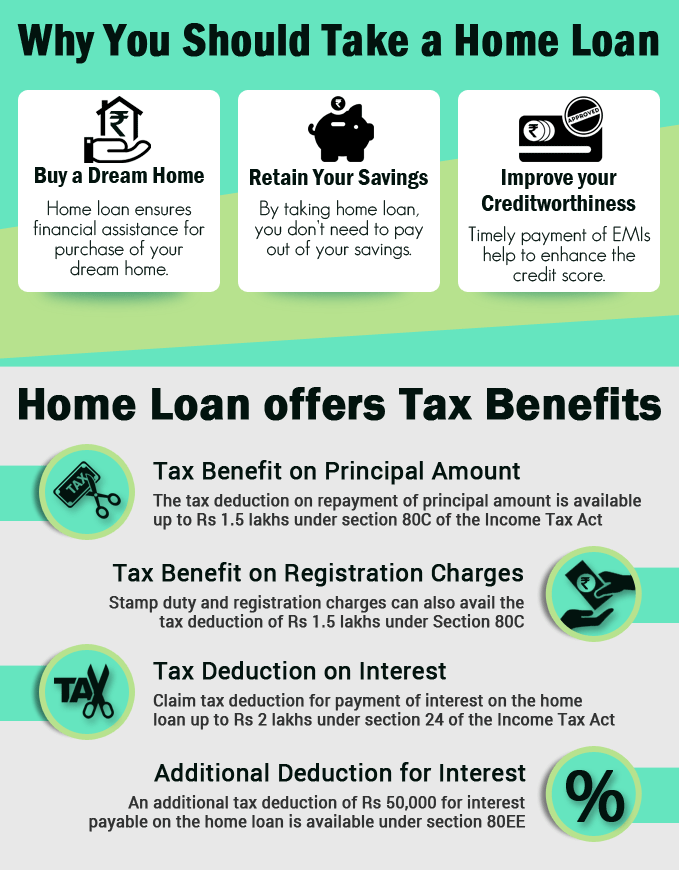

Mortgage loans are specifically designed to help individuals purchase homes. With competitive interest rates and flexible repayment terms, these loans make homeownership accessible to a wide range of people. By securing a mortgage, you can invest in a valuable asset that appreciates over time.

Education Funding

Education loans provide the financial support needed to pursue higher studies. Whether you’re attending college or pursuing advanced degrees, these loans ensure that financial constraints don’t hinder your educational aspirations. With proper planning, education loans can open doors to exciting career opportunities.

Conclusion

In summary, the benefits of a loan extend beyond immediate financial relief. They offer flexibility, improve credit scores, and provide the necessary capital for personal and business growth. By understanding the different types of loans and their associated terms, you can make informed decisions that align with your financial goals.

We encourage you to share your thoughts and experiences in the comments section below. Your feedback helps us create more valuable content. Additionally, feel free to explore other articles on our site for further insights into personal finance and business strategies. Remember, responsible borrowing is key to maintaining financial health and achieving long-term success.

Data sourced from reputable financial institutions such as Federal Reserve and Consumer Financial Protection Bureau.