Understanding how long a hard inquiry stays on your credit report is crucial for maintaining a healthy financial profile. A hard inquiry can impact your credit score and plays a significant role in your overall creditworthiness. In this article, we will delve into the details of hard inquiries, their effects, and how to manage them effectively.

Credit reports are the foundation of your financial reputation. They contain a detailed history of your financial behavior, including loans, credit cards, and payment history. One aspect that often raises concerns is the presence of hard inquiries. Knowing how they affect your credit score and how long they remain on your report is essential for anyone looking to improve their credit standing.

This article will provide an in-depth exploration of hard inquiries, covering everything from their definition to strategies for minimizing their impact. Whether you're a novice in credit management or someone looking to refine their financial strategies, this guide will offer valuable insights to help you navigate the complexities of credit reporting.

Read also:Discover Marlboro High School A Hub Of Excellence And Growth

Table of Contents

- What is a Hard Inquiry?

- How Long Does a Hard Inquiry Last?

- Effects of Hard Inquiries on Credit Score

- Soft vs. Hard Inquiry

- How Many Points Can a Hard Inquiry Drop?

- Ways to Remove Hard Inquiries

- Preventing Unwanted Hard Inquiries

- Factors Affecting Credit Score

- Best Practices for Credit Management

- Conclusion and Next Steps

What is a Hard Inquiry?

A hard inquiry occurs when a lender or creditor checks your credit report to assess your creditworthiness, typically when you apply for credit or a loan. Unlike soft inquiries, which do not affect your credit score, hard inquiries can have a temporary impact on your credit rating. Understanding the difference between these types of inquiries is essential for maintaining a healthy credit profile.

Who Can Initiate a Hard Inquiry?

Hard inquiries are typically initiated by financial institutions, such as banks, credit card companies, and auto lenders. These entities request access to your credit report to evaluate the risk of lending to you. Below are some common scenarios where hard inquiries may occur:

- Applying for a mortgage

- Requesting a new credit card

- Seeking an auto loan

- Opening a new line of credit

How Long Does a Hard Inquiry Last?

A hard inquiry remains on your credit report for two years. However, its impact on your credit score typically diminishes over time. Most credit scoring models only consider hard inquiries from the past 12 months when calculating your score. This means that while the inquiry may stay on your report for two years, its effect on your credit score is usually short-lived.

Why Does a Hard Inquiry Last for Two Years?

The two-year duration allows lenders to see a more comprehensive picture of your credit behavior. It provides insight into how frequently you apply for credit and helps them assess your financial stability. However, it's important to note that older inquiries carry less weight in credit scoring algorithms, minimizing their long-term impact.

Effects of Hard Inquiries on Credit Score

While hard inquiries can lower your credit score, the impact is generally minor. Most people experience a drop of less than five points per inquiry. However, the effect can vary depending on your overall credit history and the number of inquiries on your report.

Factors Influencing the Impact

The extent to which a hard inquiry affects your credit score depends on several factors, including:

Read also:What Does Tyt Stand For A Comprehensive Guide

- Your total number of credit accounts

- The length of your credit history

- Recent credit applications

- Your credit mix

Soft vs. Hard Inquiry

It's important to differentiate between soft and hard inquiries. While both involve accessing your credit report, they differ significantly in their impact:

Key Differences

- Soft Inquiry: Does not affect your credit score and is typically initiated by yourself or a third party for informational purposes.

- Hard Inquiry: Can impact your credit score and is initiated by a lender or creditor during a credit application process.

How Many Points Can a Hard Inquiry Drop?

The exact number of points a hard inquiry can reduce your credit score varies depending on your individual credit profile. On average, a single hard inquiry may cause a drop of 1 to 5 points. However, for individuals with shorter credit histories or fewer accounts, the impact could be slightly more significant.

Factors Influencing the Point Drop

Several factors contribute to the extent of the point drop:

- Number of recent inquiries

- Credit utilization ratio

- Payment history

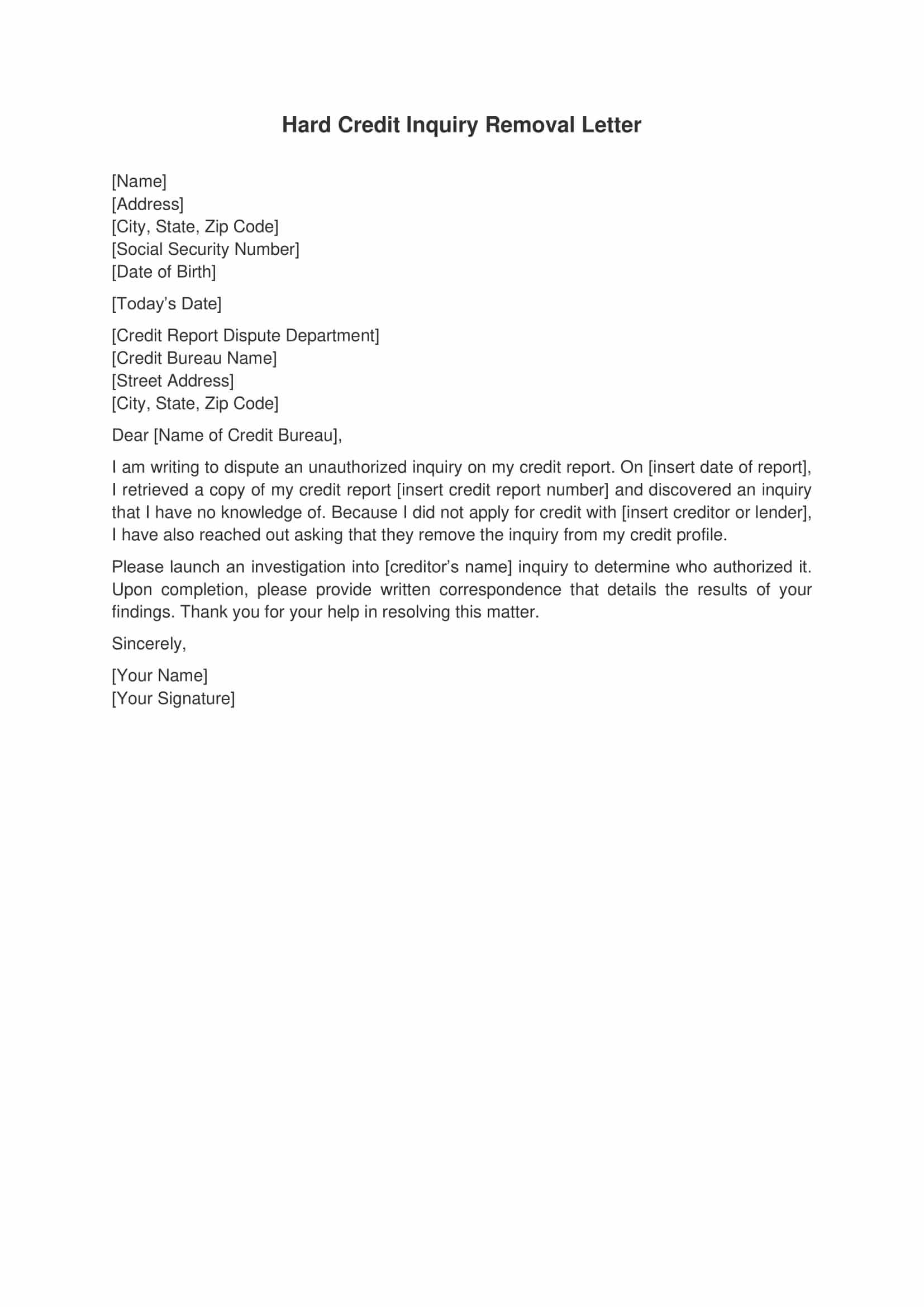

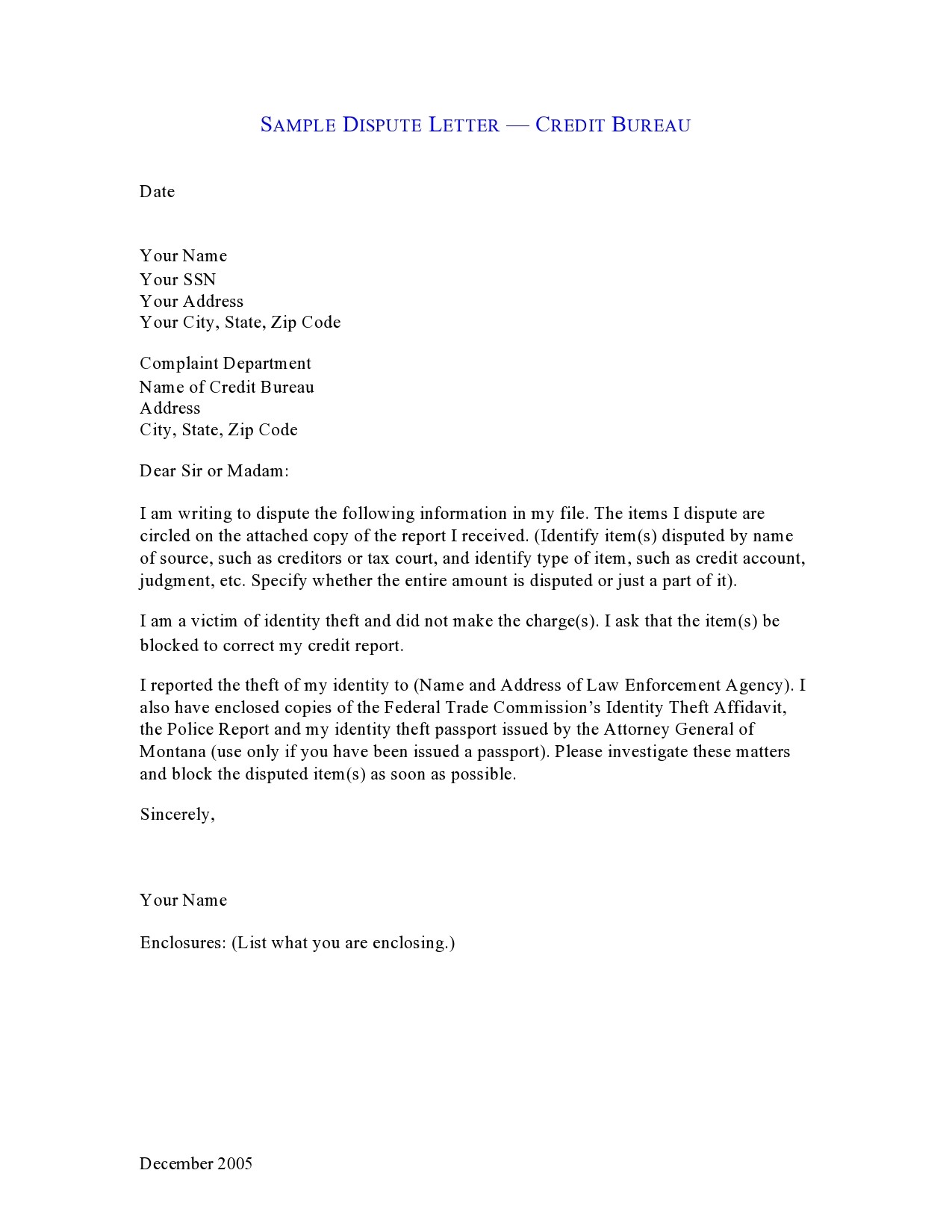

Ways to Remove Hard Inquiries

While most hard inquiries remain on your credit report for two years, there are situations where you may be able to remove them earlier. Below are some strategies for removing unauthorized or duplicate inquiries:

Disputing Incorrect Inquiries

If you notice an inquiry on your credit report that you did not authorize, you can dispute it with the credit bureau. Follow these steps:

- Gather evidence to support your claim

- Contact the credit bureau in writing

- Provide documentation proving the inquiry is unauthorized

Preventing Unwanted Hard Inquiries

To minimize the number of hard inquiries on your credit report, consider the following strategies:

- Pre-qualify for credit offers to avoid unnecessary applications

- Limit the number of credit applications within a short period

- Check your credit report regularly for unauthorized inquiries

Factors Affecting Credit Score

While hard inquiries play a role in determining your credit score, they are just one of many factors. Other key components include:

Primary Factors

- Payment history (35%)

- Credit utilization (30%)

- Length of credit history (15%)

- Credit mix (10%)

- New credit (10%)

Best Practices for Credit Management

Managing your credit effectively requires a proactive approach. Here are some best practices to help you maintain a strong credit profile:

- Pay bills on time to establish a positive payment history

- Keep credit card balances low to maintain a healthy credit utilization ratio

- Monitor your credit report regularly for errors or discrepancies

- Limit new credit applications to avoid excessive hard inquiries

Conclusion and Next Steps

Understanding how long a hard inquiry stays on your credit report and its potential impact is vital for maintaining a strong financial foundation. By following the strategies outlined in this article, you can minimize the effects of hard inquiries and improve your overall credit health.

We encourage you to take action by reviewing your credit report, disputing any unauthorized inquiries, and implementing best practices for credit management. Share your thoughts or questions in the comments below, and explore other informative articles on our website to further enhance your financial knowledge.

For more detailed information on credit reporting and management, refer to reputable sources such as the Consumer Financial Protection Bureau and the Federal Reserve.